Thanks for reading Chain Reaction! Subscribe for free to receive new posts and support my work.

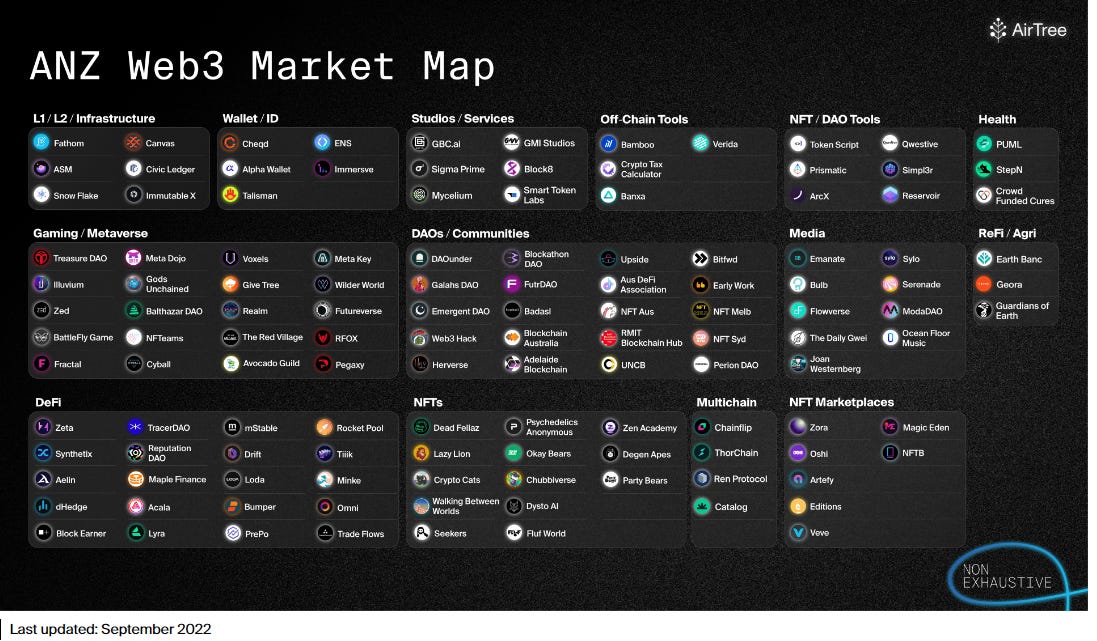

The ANZ web3 space is alive and kicking. I recently came across this overview of the companies in the space put together by Airtree.

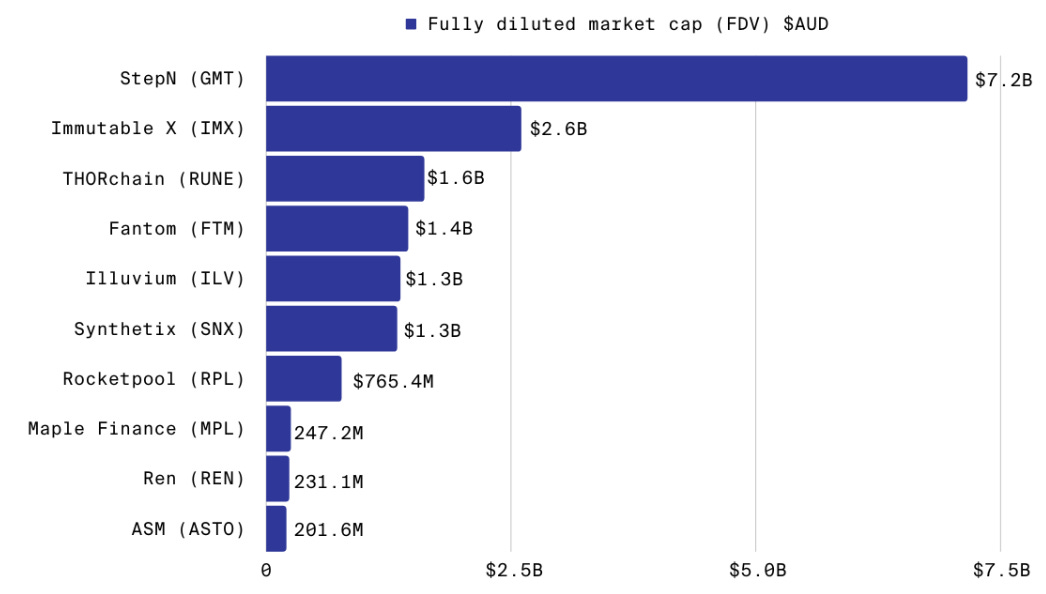

It also highlighted the Top 10 protocols in ANZ (by token fully diluted value)

I had written a detailed post on Immutable, early this year and intend to continue exploring other exciting companies from ANZ.

This post goes into Maple Finance and attempts to throw some light on

What is Maple? Who are the customers? What is its business model?

Overview of the market opportunity

Maple’s competitive advantages and significant risks it faces

Execution team and existing investors

Governance and Tokenomics

DCF valuation (quick and dirty)

Getting Rekt

According to Binance Academy

In the world of blockchain and cryptocurrencies, rekt is used to describe a severe financial loss, caused by a bad trade or investment

Okay let’s start with a game of ‘Guess Who’

Entity ‘A’ lent a whole lot of money to another entity ‘B’ that operates as an investment firm with c.$20b in assets

However, entity ‘B’ ended up making some highly dubious investment/ trading decisions.

Result: Entity ‘A’ ended up losing billions and consequently stopped the business of lending to investment firms

Guess Entity ‘A’

Any guesses? Are you thinking of crypto lending platforms?

Well - the correct answer is actually Credit Suisse! And the investment firm is Archegos Capital. Here’s a NY Times post on the matter

Credit Suisse suffered humiliation and shareholder wrath this year (2021) when it lost $5.5 billion from the collapse of the Archegos Capital Management investment fund…the bank admitted that its own failings were to blame, releasing a report that chronicled the “fundamental failure of management and controls” behind the debacle

The Credit Suisse / Archegos saga played out in mid-late 2021

Almost a year later in 2022 - we had the crypto equivalent. Here’s the story from CNBC

Three Arrows Capital managed about $10 billion in assets, making it one of the most prominent crypto hedge funds in the world….the firm, also known as 3AC, is headed to bankruptcy court after the plunge in cryptocurrency prices and a particularly risky trading strategy combined to wipe out its assets and leave it unable to repay lenders

In the crypto context, the investment firm was Three Arrows Capital and the Entity ‘A’ that lent money could be Genesis or Voyager or BlockFi.

As you can see there are plenty of alternate answers to Entity ‘A’!

What was the point of all these stories….just that lending is bloodyhard….either in TradFi or Web3!

So with that established - let’s dive into Maple Finance - a leading Australian DeFi lending platform combining transparency of DeFi and the rigour of TradFi.

I will attempt to follow my framework to review Maple Finance

What is Maple Finance

Understanding the business - What does the company do?

Founded in Oct 2020 by Sidney Powell and Joe Flanagan - Maple is based on the corporate underwriting business of traditional banks but replaces the operations team with blockchain technology.

Analogy: It’s like Shopify but for capital markets. Provides an infra layer enabling lending and borrowing - the same way Shopify provides the infra layer for people wanting to set up D2C businesses

Diagram:

As you can see from the above - Maple facilitates lending and borrowing, much like a bank, however, there are a few critical differences from a bank

Unlike a bank that makes all the credit decisions for the capital itself - in Maple’s case, it partners with external credit experts (called ‘Pool Delegates’). These experts are responsible for due diligence on borrowers and negotiating terms with them

All lending is on-chain - that basically means anyone can see who the money was lent to and on what terms

It’s an asset-light model - no branches and no significant own equity capital

Plain English:

Maple Finance is a decentralised corporate credit market. As a lender looking to put some capital to use one can get different interest rate options based on the risk of the pool.

Technical:

Maple Finance is an institutional crypto-capital network built on Ethereum and Solana. It offers (to its lenders) globally accessible, diversified fixed-income yield opportunities by lending to a pool of premium crypto institutions

Product-market fit - Who is it doing it for? Is there really a need?

Let’s first see who it’s not targeted at….Here’s Sidney Powell (CEO and Co-founder, Maple)

We’re not a product that’s marketed to mums and dads as a replacement for a bank account…

..You’re doing term loans to credit, and it’s being underwritten to achieve a high single digit (return) after any losses from defaults. At the end of the day, these loans carry credit risk

Maple primarily targets institutional borrowers - corporates with established businesses and demonstrated cashflows.

Typically the borrowers are capital-intensive businesses - the most prevalent being market makers and high-frequency traders.

Here is Byrne Hobart explaining market makers in TradFi context

Even if there are buyers and sellers, they may not be willing to transact and precisely the same terms and at exactly the same moment.

A market-maker is a wholesaler, willing to store inventory between when a seller needs to get rid of it (shares) and when the next buyer comes along

Typical lending product on the platform - Fixed term Fixed rate loan

Size: $5-15m

Term: 6 months

Interest rate: 8.5% - 12.5%

Collateral level: nil to 10%

The business is targeting sophisticated lenders like Family offices, HNIs who may want to deploy excess liquidity and understand the associated risks.

A lender can expect rates ranging from 5% - 10% APY (comparable rates on AAVE and Compound would be c.0.5%)

The returns are much higher as lenders are exposed to the credit risk of the borrower on Maple.

In case you are wondering if there is demand for this service…

…here is a chart showing how the value of loans lent by Maple protocol

Dune Analytics

Value of loans outstanding has grown from c.$20m in Jun 2021 to c.$300m in Sep 2022 and rising as high as $800m in Jun 2022.

Business model - How does Maple make money?

Maple protocol revenue is derived from Loan establishment fees paid by borrowers for each loan originated on Maple (primary revenue source)

Establishment fees are 0.99% annualised and two-thirds, or 66bps, is paid to the Maple Treasury, and one-third, or 33bps, is paid to the Pool Delegate that issues the loan.

The protocol share is then used to pay for operational expenses like salaries, marketing, admin, etc.

Also here is a great video by Joe Flanagan (Maple co-founder) explaining the business model

What is the opportunity?

The blue-sky opportunity just by comparison to TradFi is immense.

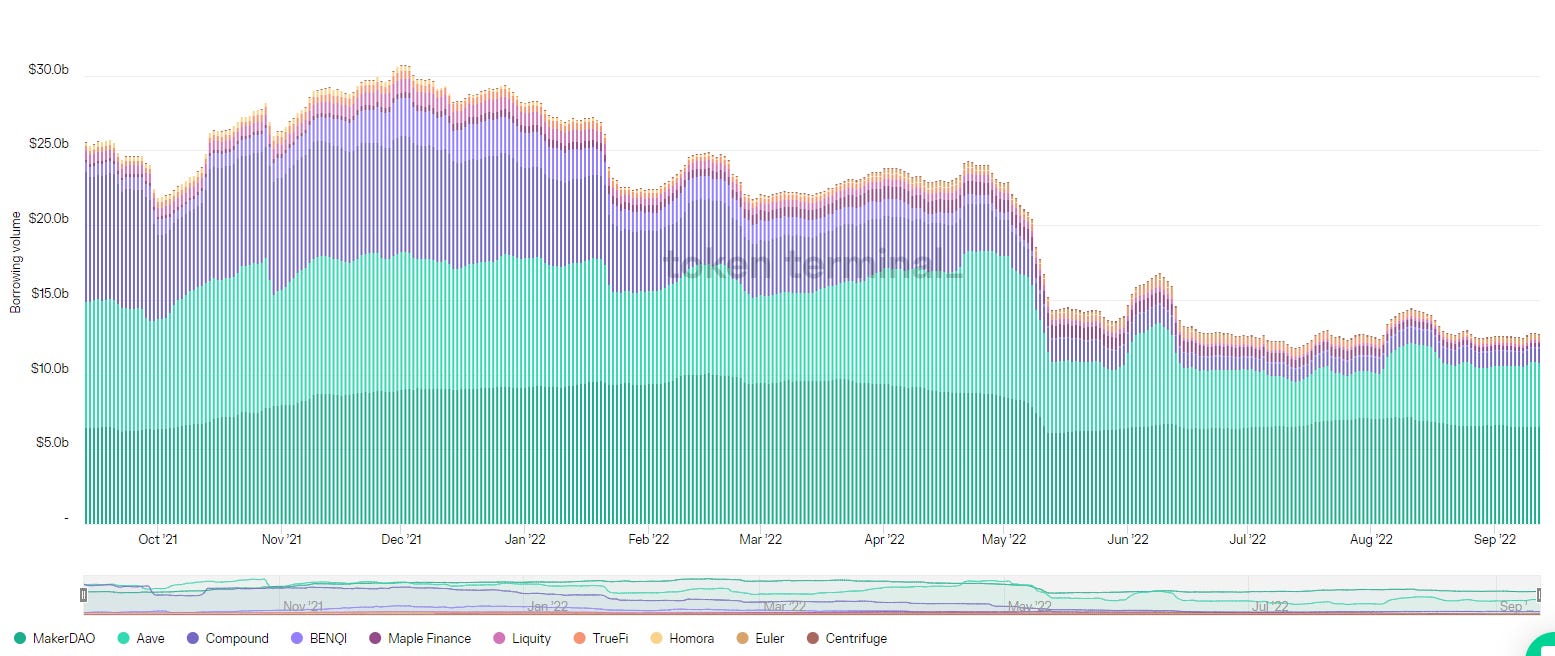

However, first let’s consider the current state of crypto lending markets.

Crypto lending markets represent a large market opportunity. The total borrowing value for the global lending markets stood c.$12bn as of Sep 2022, having topped $30bn in Dec 2021.

Okay let’s have a look at the lending landscape in crypto (not exhaustive - only indicative)

Above matrix attempts to put lenders into buckets based on the level of collateral required to borrow on the platform and the degree of decentralisation of the platform.

Most DeFi lending requires high level of collateral i.e. you transfer $100 worth of asset to the protocol and get back $70 worth of loan. While this is a nice-safe approach - it’s not capital efficient.

Generally, CeFi lending also requires high levels of collateral.

These approaches work well if you have a ton of bitcoin/Eth already and are able to borrow USDC against it. However, it’s easy to imagine a lot of businesses/entities do not have large amounts of crypto lying around.

Most of the lending volume (90%+) is dominated by the DeFi lenders (Maker Dao, Compound, AAVE) requiring high levels of collateralisation / overcollateralisation.

Maple is filling the market gap for a DeFi lender that provides loans without any or very low requirements for collateral.

Competitive strengths and risks

Unique offering:

As we saw in the market map - currently, uncollaterised loans are an underserved market representing a huge opportunity.

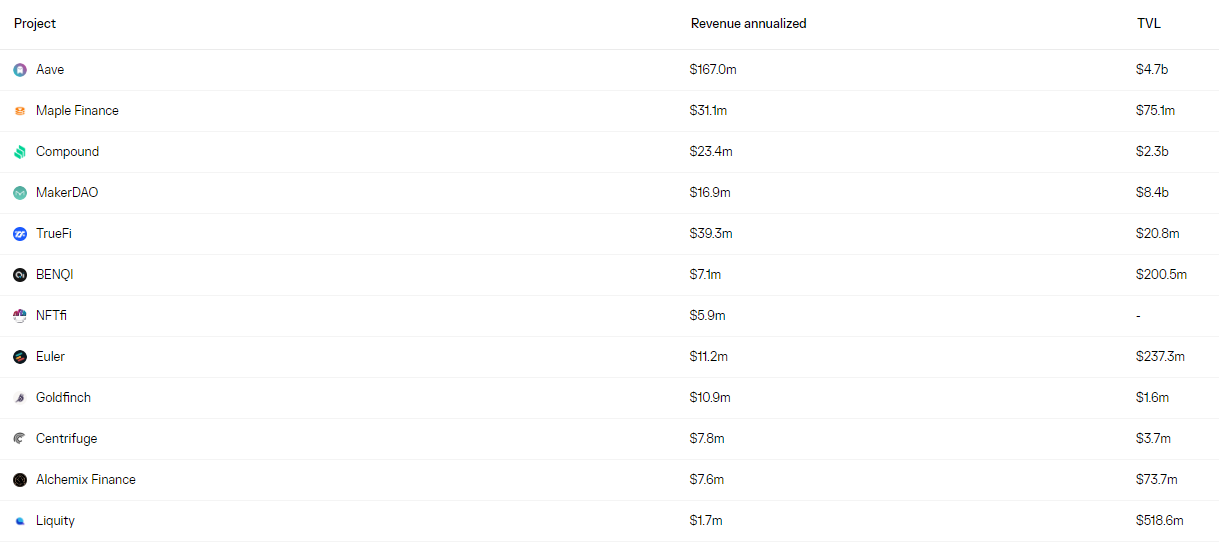

#2 lending protocol based on revenues:

Despite having a much lower TVL (Total Value Locked) as compared to the larger players - Maple ranks #2 by annualised revenues

Source: Token Terminal

Several growth pathways:

New chains: Maple started on Ethereum and now has expanded onto Solana. In future, it could expand to L1s/L2s

New verticals:

Within Crypto: Plans to expand lending services to bitcoin mining community in Q3 CY2022

Outside crypto: Expand to Fintech / SaaS corporates

New products: Plans to offer new lending products other than the fixed rate/term loans

Easy to use interface and transparency:

The website is super well laid out and easy to understand. The dashboards are intuitive and give the necessary information. Below is an example of Maven pool

Maple website

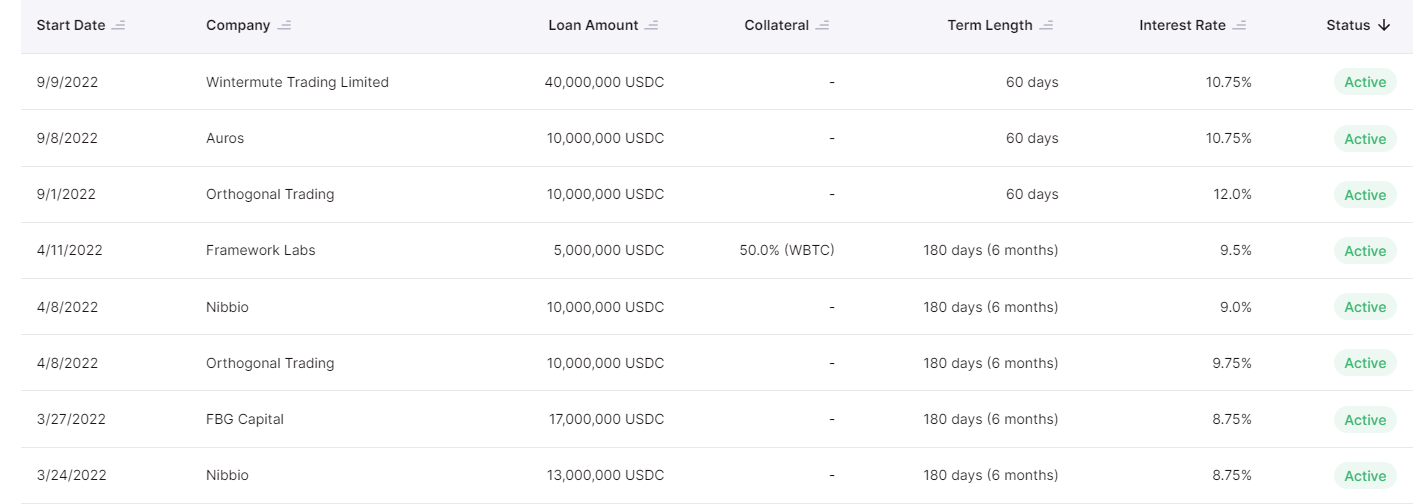

A lender can clearly see who the borrower is within any pool and on what terms and also if there is any concentration risk within the pool.

Maple website

Focus on processes resulting in good operating metrics:

Robust processes in place to screen and on-board

Pool delegates: All pool delegates go through a thorough vetting process. They are typically funds and industry professionals with credit experience

Borrowers: Need to clear KYC/AML checks. This is followed by more traditional due diligence checks - review of P&L, Balance sheet, business plans etc. Here’s an overview of risk assessment criteria

Maven deck

Risks

Quality of pool delegates: Maintaining the quality of pool delegates is critical as they are in charge of the credit appraisal and negotiating terms with lenders. The quality of the loan book depends on the quality of the pool delegates

Scaling: The human element within the credit check process places natural limitations on scaling. How effectively Maple is able to partner with pool delegates targeting different verticals remains to be seen

Quasi B2B business model potentially requiring large sales force: Convincing sophisticated lenders to come onboard is more akin to a B2B SaaS model which requires a skilled and large sales force. Will Maple manage to find innovative ways to grow without investing a huge amount in the sales team?

Sidney has a background in debt securitisation and has previously worked at NAB. Joe also has a background in finance having held a leadership position with Clover Advisory and worked with PwC.

Both were irked by the long and laborious process to raise debt for a corporate and decided they were going to do something about it.

Over the last couple of years, they have attracted a raft of high-profile investors including Framerwork Ventures, Polychain Capital, Koji Capital, Kain Warwick (Founder, Synthetix), Stani Kulechov (Founder, Aave)

Decentralisation, Governance & Tokenomics

If we were to think of decentralisation based on the below factors..

i) Transparency: Ability for anyone to see details of loans, terms, etc. (by being on-chain)

ii) Permissionless: Ability for anyone to join the platform as a lender/borrower

iii) Governance: Decentralised via a DAO or done more centrally by the management team

…we could come up with below spectrum

Being on-chain Maple scores pretty high on transparency. However, unlike Aave, Compound - it is not fully permissionless.

This is by design ofcourse.

Aave and Compound operate a overcollaterised loan book - which allows them to be permissionless.

To be able to provide a undercollaterised loan product Maple has decided to combine the rigour of TradFi credit function with the transparency of the DeFi world.

Governance

The corporate structure of this crypto entity comprises MPL holders, the Maple DAO, and an operating entity.

MPL is the governance token of the Maple Protocol. It enables holders to participate in governance, earn fees, and provide pool cover.

Tokenomics

I find it useful to apply the framework Nat Eliason came up with to review crypto asset tokenomics. Here’s Nat on the importance of Tokenomics

“Tokenomics” has become a popular term in the last few years to describe the math and incentives governing crypto assets. It includes everything about the mechanics of how the asset works, as well as the psychological or behavioral forces that could affect its value long term.

Projects with well-designed tokenomics are much more likely to succeed in the long term because they’ve done a good job of incentivizing buying and holding their token.

Here’s Maples’ pathway to 10m from Messari. It is expected to reach that number by Apr 2023.

Based on the above schedule, by Sep 2022 - c.85% of tokens have been released.

So - not a whole lot of emissions left - however, by Apr 2023 all tokens would be unlocked.

Another way of looking at this is that the earnings need to increase by atleast 15-17% over the next 6 months to keep pace with new token issue - which doesn’t seem unrealistic/insane.

Demand drivers:

Main question that we need to understand is - what’s the utility of owning the MPL token?

MPL has two main utilities

ROI potential - there are two avenues to earn

Staking income: MPL holders who stake their tokens will get a share of the protocol revenues (c.10% APY)

Pool cover income: MPL holders who contribute their tokens into a ‘cover pool’ - essentially an insurance pool to cover for borrower defaults will earn an additional income (8 - 10% APY)

Governance rights - as we discussed MPL holders have the ability to influence the running of the protocol by voting on different governance proposals

Maple has demonstrated a track record of generating real revenues and MPL token is an instrument to get you a share of those revenues - this is the biggest incentive for people to continue holding the token.

Additionally, it also provides governance rights which provides the additional reason (although not as strong as share of revenues) to increase demand for the token.

Like for any TradFi business - one can make assumptions about revenue, margin profile, capex and formulate an intrinsic value of the business using a cashflow model

Maple does a relatively good job of reporting its financials. However, to do a high-quality DCF we’d need a lot more information plus access to management plans - but we can attempt a quick and dirty DCF!

Now for the disclaimer - the idea of this exercise is just to illustrate that with adequate information a DCF is possible. These are based on a variety of SIMPLIFYING assumptions (I won’t go into them here, hit me up separately if you would like to discuss them)

Final word

The vision of the founders is to become a capital market infra layer that enables credit experts around the world to break away from TradFi and start their own lending practice.

So far they have built an incredible business in a short time and I feel they are well-placed to take on the challenges that no doubt will come their way.

Look forward to closely following their journey!

Thanks for reading Chain Reaction! Subscribe for free to receive new posts and support my work.